In a massive healthcare breakthrough in the race to save and protect lives from COVID-19, Pfizer has announced some highly promising vaccine trail results. All going to plan, this should save lives, and in time, help return our societies to some form of normality.

While it’s not yet a finished product, the vaccine shows great promise and is close to the mark, with large-scale testing that hasn’t shown side effects. Extrapolating this forward, we might be able to contain the COVID-19 virus more than the flu, even if it mutates.

Why markets are watching

Markets of course are also interested in reflecting this panacea, as it could mean increased mobility and reopening for society and all the spending that entails. A vaccine could also potentially be a contributing factor to the end for deflation. Both are powerful forces that can push equity profitability higher.

In our view, it won’t be a straight line upwards, but the surge of optimism (and short covering) on Tuesday, 11 October in Australia, could show the path forward as the world emerges from a tough year.

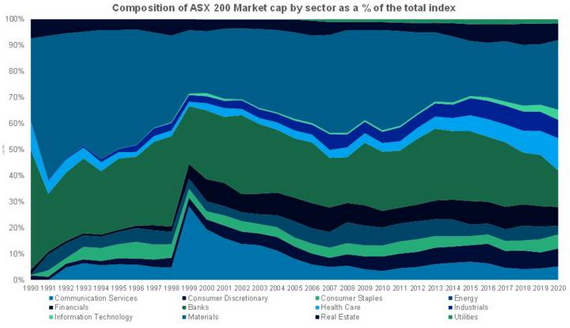

Sectors that led the vaccine rally Travel, Banks and Energy are coming off all-time lows of market cap share.

Source: AMP Capital, Bloomberg. Note travel stocks are a subset of both industrials and consumer discretionary sectors.

The winners so far

Sectors like travel, energy and banking that were at their lowest quarterly proportions of our ASX200 index at the beginning of this quarter are amongst the biggest gainers of the vaccine’s boost so far.

For background, since the pandemic hit, energy has lacked demand and had weak commodity prices across oil, gas and electricity. Banks have had low margins and credit growth, both of which have bottomed and are going higher in our market. Travel stocks of course have suffered with tourism being depleted.

These three poster child value sectors are now so cheap that they might offer high EPS (earnings per share) growth, as much lower valuations than you can get in the growth side of the market and that is why we believe they can make sustained gains as the virus is forced to retreat.

Could there be losers?

The losers from a vaccine on the market could perversely be those that have gained most this year:

-

Tech disrupters which had been gaining not on profitability but on the promise of it down the line (assuming they are not disrupted by the next wave of technology by then) after a fast transition to a digital and contactless COVID-19 world;

-

Some health care stocks which provided PPE equipment or ventilators for the outbreak; and

-

Online shopping which had enjoyed a massive boom as people shopped from their homes.

With the shift of earnings growth back into real businesses, some of these growth valuations are hard to justify and may push valuation multiples lower as the rate of change of customer adoption turns negative. The run up in valuations in tech has been overdone and there are real risks to their stock prices here if revenue trends moderate.

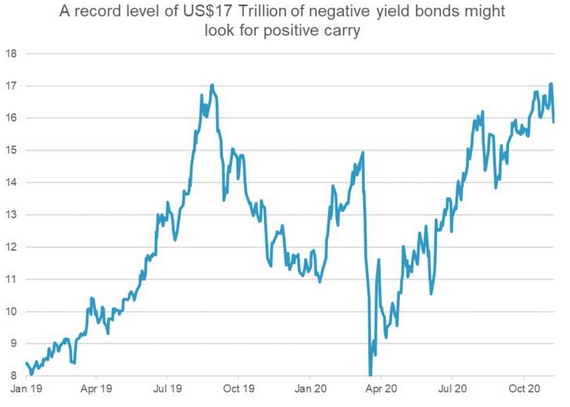

Source: AMP Capital; Bloomberg

Then of course there is the challenged alternatives-to-equities in a low-rate world. Would you believe that there are currently US$17 trillion in bonds with negative yields in the world right now? That’s 12 times the size of our Aussie equity market, or about the same market cap as all stocks currently listed on the New York Stock Exchange. This is because of zero interest rates, risk aversion and a lack of safe assets.

Importantly too, should the vaccine inoculate inflation and boost growth, we should start to see a rotation of investments out of these bonds (which are a cost to hold) and into equities that are reasonably valued and broadly recapitalised.

As we get closer to a widespread vaccination plan, we will see these trends continue and it could be a great shot in the arm for equity returns in 2021.

Author: Dermot Ryan Co-Portfolio Manager, Sydney, Australia

Source: AMP Capital 18 Nov 2020

Reproduced with the permission of the AMP Capital. This article was originally published at AMP Capital

Important notes: While every care has been taken in the preparation of this article, AMP Capital Investors Limited (ABN 59 001 777 591, AFSL 232497) and AMP Capital Funds Management Limited (ABN 15 159 557 721, AFSL 426455) (AMP Capital) makes no representations or warranties as to the accuracy or completeness of any statement in it including, without limitation, any forecasts. Past performance is not a reliable indicator of future performance. This article has been prepared for the purpose of providing general information, without taking account of any particular investor’s objectives, financial situation or needs. An investor should, before making any investment decisions, consider the appropriateness of the information in this article, and seek professional advice, having regard to the investor’s objectives, financial situation and needs. This article is solely for the use of the party to whom it is provided and must not be provided to any other person or entity without the express written consent of AMP Capital.

This article is not intended for distribution or use in any jurisdiction where it would be contrary to applicable laws, regulations or directives and does not constitute a recommendation, offer, solicitation or invitation to invest.